What is an HSA?

Tax-favored HSAs can only be established by eligible individuals who are covered by a high- deductible health plan (HDHP) and not covered under any other health plan which is not an HDHP, unless the other coverage is permitted insurance or coverage for accidents, disability, dental care, vision care, or long-term care. Eligible individuals may, subject to statutory limits, make contributions to HSAs, and employers as well as other persons (e.g., family members) also may contribute on behalf of eligible individuals. (Code Sec. 106, Code Sec. 223)

An account holder gets the deduction for contributions to his HSA even if someone else (e.g., a family member) makes the contributions. (Code Sec. 62(a)(19)) Employer contributions to an HSA are excludable from the employee's income – so these contributions are not deducted on the employee’s tax return. Distributions for qualifying medical expenses are tax-free but these same medical expenses cannot be used as a Schedule A medical deduction.

Contributions to HSAs (other than employer contributions) are an above-the-line deduction, amounts in an HSA may be accumulated tax-free, and distributions are tax-free if used to pay or reimburse qualified medical expenses. Many of the rules related to HSAs are similar to rules that apply to IRAs and Archer Medical Savings Accounts.

An HSA is a tax-exempt trust or custodial account established exclusively for the purpose of paying qualified medical expenses of the account beneficiary who is covered under a high-deductible health plan (defined below). Coverage under a high-deductible health plan is looked at on a month-by-month basis.

Eligible Individual

To be eligible to establish an HSA, an individual, for any month:

-

Must be covered under a high-deductible health plan (HDHP) on the first day of the month;

-

Is not also covered by any other health plan that isn’t an HDHP, except certain permitted coverage (see below);

-

Is not entitled to benefits under Medicare (i.e., generally individuals who haven’t yet reached age 65); and

-

Is not claimed as a dependent on someone else’s return.

Health Flexible Spending Accounts (FSA) & HSAs

A health FSA (Code Sec 213), offered by an employer, as part of the employer’s qualified cafeteria plan, allows employees to contribute up to $3,300 (2025) in pretax dollars annually to be used by the individual to pay medical expenses of the individual, their spouse and dependents during the year. Unused amounts are generally forfeited. However, the plan either can have a grace period of up to 2½ months after the end of the plan year in which to use up the unused amount or allow up to $660 (up from $640 in 2024) of unused amounts from the end of the plan year to be used to pay or reimburse qualified medical expenses in the following year. Unused amounts in excess of the carryover amounts are forfeited (cannot be returned to the employee). The carryover amount does not reduce the maximum contribution amount allowed for the carryover year.

There are two types of health FSA plans:

-

General Purpose Health FSA – One that reimburses all qualified medical expenses without restriction that is classified as a “health plan that constitutes other coverage” and having such coverage would make the individual ineligible to make contributions to an HSA.

-

HSA-compatible Health FSA – One that is a limited-purpose health FSA, a post-deductible health FSA, or a combination of the two.

HSAs Are Not Limited to Employer Plans

There are many different custodians who can manage the contributions (search the web for “HSA custodians”). Thus, if the taxpayer has a qualifying HDHP they can contribute to HSA even if they do not have earned income.

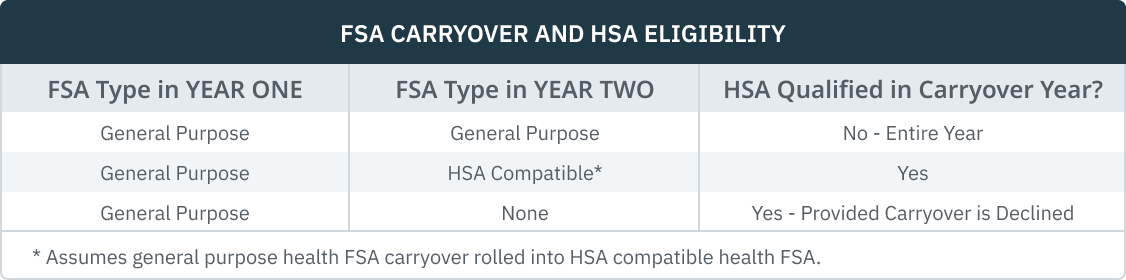

FSA Carryover and HSA Eligibility

The impact of health FSA carryover from one year to the other on HSAs is dealt with in Chief Counsel Advice 201413005. The following is a synopsis of the Chief Counsel’s advice where there is carryover from year 1 to year 2:

Medicare Coverage

IRS has interpreted being “entitled to benefits under Medicare” to mean both eligibility and enrollment in Medicare. An individual who is otherwise eligible, but who is not actually enrolled in Medicare Part A, may contribute to an HSA until the month actually enrolled in Medicare. (IRS Notice 2004-50; IRS Notice 2008-59) If an individual has delayed applying for Medicare, when they do apply, their enrollment may be back dated (retroactive) for up to 6 months. Thus, any contributions made to their HSA during the period of retroactive coverage will be considered excess contributions. (IRS Pub 969) Accordingly, those with an HSA who plan to delay enrollment in Medicare should stop making contributions to their HSA at least 6 months before Medicare enrollment to avoid a tax penalty for excess contributions.

VA Coverage

An individual who is eligible to receive Department of Veterans Affairs (VA) medical benefits will be treated as an eligible individual if otherwise qualified and no VA medical benefits have been received during the preceding three months. The 3-month rule does not apply if the medical benefits consist solely of disregarded coverage (defined below) or preventive care. (IRS Notice 2008-59)

Indian Health Service (IHS)

An individual who is eligible to receive medical services at an IHS facility, but who has not actually received such services during the previous three months, is an eligible individual within the meaning of § 223(c)(1) who may establish and make tax-free contributions to an HSA. However, an individual generally is not an eligible individual if the individual has received medical services at an IHS facility at any time during the previous three months. Notice 2004-2, Q&A-6, provides that the receipt of permitted coverage, such as dental and vision care, or the receipt of preventive care, such as well-baby visits, immunizations, weight-loss and tobacco cessation programs, does not affect an individual’s eligibility. (IRS Notice 2012-14)

Other Allowed Insurance

An individual will not be prevented from establishing an HSA if, in addition to an HDHP, the individual has coverage for benefits provided by “permitted insurance,” under which substantially all the coverage provided relates to:

-

Worker’s compensation laws;

-

Tort liabilities;

-

Liabilities relating to ownership or use of property, such as automobile insurance;

-

Insurance for a specific disease or illness, such as cancer insurance; and

-

Insurance that pays a fixed amount per day (or other period) of hospitalization.

In addition, eligibility for an HSA will not be compromised merely because the individual also has coverage (whether provided through insurance or otherwise) for accidents, disability, dental care, vision care, or long-term care—collectively termed “disregarded coverage”. Discount cards entitling the holder to discounts for health care services or products at managed care market rates will not disqualify the individual from being an eligible individual for HSA purposes, if the individual is required to pay the health care costs until the high-deductible health plan’s deductible is satisfied.

State Required Coverage

Generally, if a state requires a health plan to provide certain benefits without a deductible or at a deductible that is less than the minimum annual deductible, the plan may not be an HDHP.