California Differences - Recovery Rebate Credit

California Middle Class Tax Refund – Effective 2022

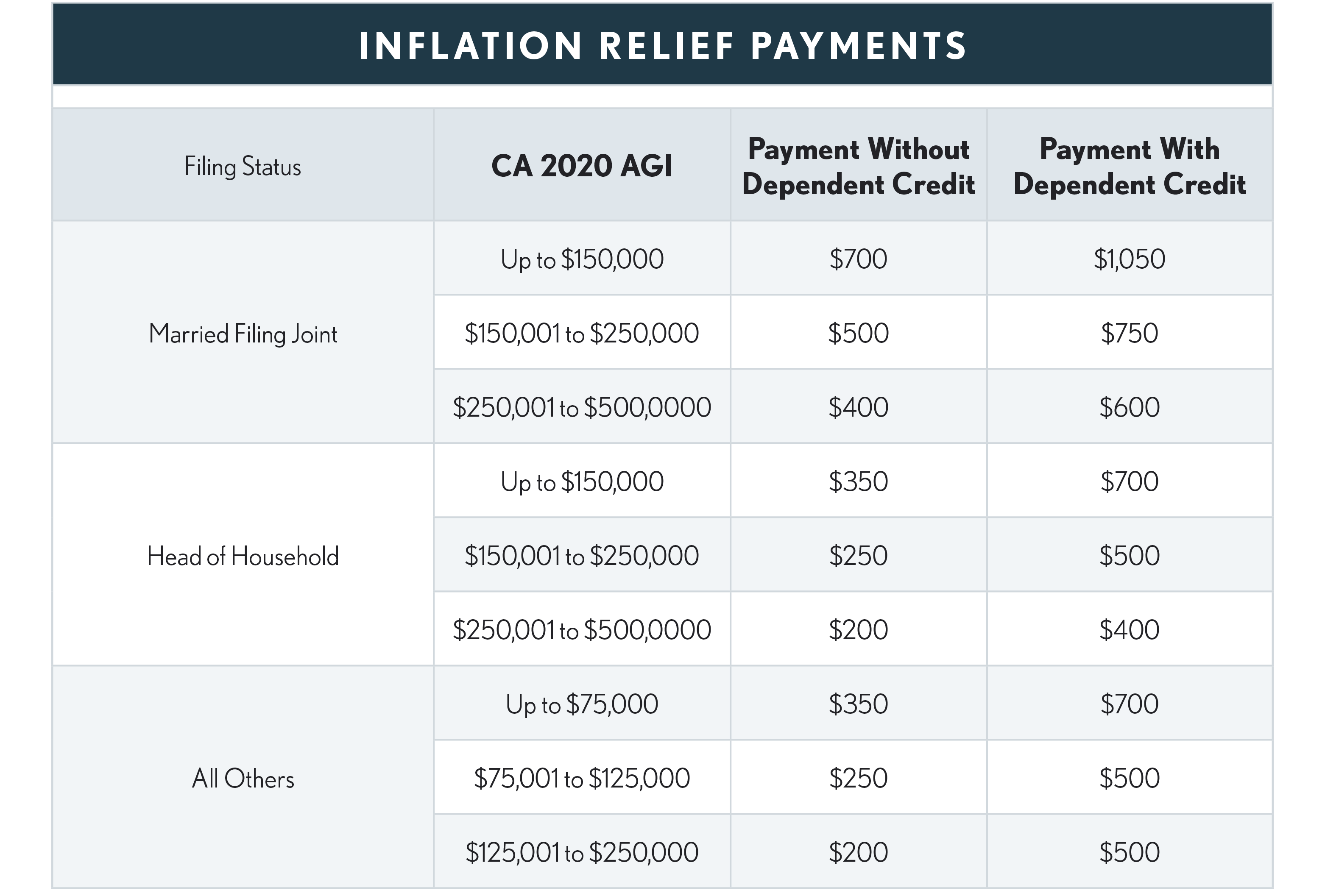

As a result of the passage of AB 192 on June 30, 2022, millions of Californians are set to get "inflation relief" payments that are included in the 2022-23 state budget. The Franchise Tax Board is calling these payments “The Middle-Class Tax Refund”. Around 23 million Californians will receive the following direct payments:

Qualifications -

-

The relief payments are based upon the taxpayer’s 2020 AGI;

-

Must be a California resident on the date the payment is issued;

-

Must have been a California resident for at least six months during 2020;

-

Must have filed their 2020 tax return by October 15, 2021*; and

-

Cannot have been claimed as a dependent on someone else’s 2020 CA tax return.

-

Individuals deceased on the payment date don’t qualify.

-

Incarcerated individuals don’t qualify, other than if incarcerated pending the disposition of charges, in a jail, prison, or similar penal institution or correctional facility on the date the payment would otherwise be issued.

*Exception: if the taxpayer applied for an ITIN and had not received it by October 15, 2021, that taxpayer must have filed a complete 2020 tax return by February 15, 2022.

These payments are exempt from garnishment orders other than a garnishment order in connection with an action for, or a judgment awarding, child support, spousal support, family support, or a criminal restitution payable to victims.

The bill excludes the payments from the gross income of recipients for California personal income tax purposes.

Per the FTB’s website, the one-time payments will begin in late October with all payments issued by early 2023.

Taxpayers will receive either a direct deposit payment or a payment by debit card, with payments by direct deposit if the return was e-filed and indicated direct deposit on the return. Otherwise, the payment will be made by debit card.

Debit Card Mailings Appear to Be a Scam - Many say the cards look like a scam since the envelope’s return address is Omaha, NE and the card is from a New York Bank. Good reasons to be skeptical with all the scams that are going around these days.

Wonder how many have tossed the envelopes in the trash without opening them?

Well, it is not a scam, and these cards are the one-time payment. The FTB website includes information about these debit cards

CA Issuing 1099-MISC – According to its website, the FTB states that the payments “may be considered federal income” and that as a result, it will issue Form 1099-MISC for any payment of $600 or more.

Is the Payment Federally Taxable? – Even though IRC Sec 61 specifies that all income, regardless of its source is taxable unless specifically excluded from income, the federal general welfare exception may apply.

The Federal General Welfare Exception is not part of the IRC, but rather has evolved from case law. Generally, to qualify a payment must be:

1. Made from a governmental fund,

2. Be for the general welfare of individuals or families, which is defined by Notice 2002-76 as payments to help individuals and families meet disaster-related expenses, and

3. NOT for payment for services.

CSEA Analysis

The CA Society of Enrolled Agents recently published a detailed analysis by David Fogel, EA, CPA with respect to the application of the federal general welfare exception to the Middle-Class Tax Refund.

The Senate and Assembly legislative analyses of the bill state that the purpose of the payment is “to provide financial relief for economic disruptions resulting from the COVID-19 emergency, such as the financial burdens of inflation and increasing costs for gas, groceries, and other necessities.” On March 13, 2020, President Trump declared the COVID-19 pandemic as a federal disaster.

Where the payments are made to individuals with an AGI as high as $500,000, it may not seem to be based upon need. However, Notice 2002-76 states that “need” is not defined in terms of financial need and that “the general welfare exclusion applies equally to all residents of an affected area regardless of their income levels.”

Thus the payments appear to meet the requirements for the Federal General Welfare Exception. If you (and your client) agree that the income isn’t federally taxable, and the client receives a 1099-MISC from the FTB:

1. Enter the 1099-MISC amount as “other income” on 1040 Schedule 1, line 8z – describe as “CA Middle Class Tax Refund” and

2. Back the same amount out as an “other adjustment” on 1040 Schedule 1, line 24z – describe as “Federal General Welfare Exception.”

Golden State Stimulus (GSS) Payments - Applied to 2020 Only

CA has authorized two stimulus payments. The GSS I and the GSS II. Qualifications are quite different for each and will not be paid until after the taxpayers file their 2020 tax returns. This is because qualifications for both are dependent on the results of the 2020 CA tax return. GSS payments are not taxable for CA purposes.

GSS Payment # 1 - Legislation (SB 88) authorized the creation of the Golden State Stimulus Emergency Fund to be used to provide one-time Golden State Stimulus (GSS I) payments and grants of $600 or $1,200. By early May 2021 the FTB announced 2.5 million GSS I payments worth $1.6 billion had been issued to eligible taxpayers in the following groups who had filed their 2020 returns from January 1 through April 22, 2021:

-

$600 to people filing with a Social Security number and claiming and receiving the California Earned Income Tax Credit (CalEITC).

-

$1,200 to people filing with an Individual Taxpayer Identification Number (ITIN) who claimed and received CalEITC.

-

$600 to taxpayers filing with an ITIN and not qualifying for CalEITC but whose CA AGI was $75,000 or less in 2020.

To qualify for the GSS I payments, 2020 state income tax filers must:

-

Have lived in California for more than half of the 2020 tax year.

-

Be a California resident on the date the GSS I payment is issued.

-

Not be eligible to be claimed as a dependent on someone else’s tax return.

For 2020 returns filed on or after April 23, 2021, and by October 15, 2021, FTB will issue payments after eligible 2020 tax returns are processed. Eligible filers should allow up to 45 days for payment if they use direct deposit. Paper checks may take up to 60 days.

GSS Payment # 2 - Additional legislation (SB 139, approved by the governor July 12, 2021), provides for a second stimulus payment (GSS II) paid as follows:

-

$600 payments to all eligible taxpayers who did not receive a first payment.,

-

Additional $500 in payments to families with dependents.,

-

Additional $500 in payments to undocumented families.

Requirements to receive a GSS II payment:

-

File 2020 tax return by October 15, 2021. (Exception: the required filing date is extended to February 15, 2022, if an individual or their spouse applied for an ITIN but didn’t receive the ITIN by October 15, 2021.)

-

Have 2020 California Adjusted Gross Income (CA AGI) of $1 to $75,000 ($37,500 MFS).

-

Have 2020 wages subject to withholding of $75,000 ($37,500 MFS) or less (this means individuals with no wages will qualify if the other requirements are met; there is no requirement to have earned income).

-

Be a California resident for more than half of the 2020 tax year.

-

Be a California resident on the date payment is issued.

-

Cannot be claimed as a dependent by another taxpayer.

GSS II payments (either direct deposit or by check) began in September 2021.

No Return Reconciliation – Unlike the federal Economic Impact Payments that are advances of the Recovery Rebate Credit, and that require a reconciliation on the 2020 and/or 2021 tax returns, GSS I and GSS II payments are economic relief payments in the nature of public assistance payments. They are not associated with a tax credit.

Therefore, they will not need to be reconciled on any California return.

Other SB 139 provisions:

-

The FTB is required to provide tax returns or tax return information to the state Controller that is necessary to make the payments. The Controller and any current or former officer, employee, agent becomes subject to existing law that prohibits unauthorized use of tax return information.

-

The Controller, until January 1, 2023, is prohibited from offsetting delinquent accounts with the GSS payments.

-

The Franchise Tax Board, until January 1, 2023, is prohibited from issuing orders to financial institutions, persons or entities to withhold and remit GSS payments to satisfy taxpayers’ obligations.

-

The Controller is to make the GSS payments by July 15, 2022.

Federal Taxation: Assuming the IRS accepts these payments as “public assistance payments” they probably will not be taxable for federal purposes. However, as of the publication date of the Big Book the IRS has not provided any specific guidance