Qualified Property For 199A Deduction

A complete list of what constitutes qualified property for the 199A tax deduction. Remember, ask a local tax professional for assistance if you have any questions about your federal business taxes.

Qualified property is defined as meaning tangible, depreciable property which is held by and available for use in the qualified trade or business at the close of the tax year, which is used at any point during the tax year in the production of qualified business income, and the depreciable period for which has not ended before the close of the tax year (Code Sec. 199A(b)(6)(A)). Qualifying tangible depreciable property would include, for example:

-

Machinery

-

Tools

-

Vehicles

-

Residential Buildings (but not land; land is not depreciable)

-

Home office (if using the actual expense method, see below)

-

Commercial Buildings (but not land; land is not depreciable)

-

Office furnishings

-

Computer systems

-

Bundled software (sold with the computer)

-

Over the counter software

-

Qualifying property (leasehold improvements, restaurant property and retail improvement property)

-

Racehorses

-

Certain fruit and nut trees and vines (once they reach production stage)

-

Certain livestock (generally those purchased for draft, breeding or dairy)

-

Farm buildings (but not land; land is not depreciable)

-

See IRS Publication 225 for other depreciable farm property

-

See IRS Publication 949 for other depreciable property

NOT included would be Sec. 197 intangibles such as:

-

Goodwill and going concern value

-

Workforce in place

-

Know-how

-

Customer and supplier-based intangibles

-

Government licenses and permits

-

Franchises, trademarks, trade names

Special Circumstances - Placed in Service Date

• MACRS property acquired in Sec 1031 Exchange or involuntary Conversion - Split Basis:

o Exchanged Basis - Date placed in service will be date the relinquished property was placed in service.

o Excess Basis – Date the replacement property was placed in service.

• Acquired in Sec 1031 Exchange or involuntary Conversion – Electing Out of Split Basis - Date the replacement property was placed in service.

Unadjusted Basis Immediately After Acquistion (UBIA)

Generally means cost or other depreciable basis on the date placed in service. (Code Sec. 199A(b)(6)(B)(3)).

-

It is not reduced for depreciation.

-

It is not adjusted for any tax credits allowed.

-

Not reduced for bonus depreciation.

-

Not reduced for Sec 179 expensing.

-

It is reduced for any personal use during the year – such as personal use of a vehicle.

-

In the case of real property, it does not include land.

-

Improvements are treated as separate qualified property.

-

Property is not qualified property if acquired within the last 60 days of the year and disposed of within 120 days without being used for at least 45 days prior to disposition. However, ok if taxpayer can show the purposes was not to increase the 199A deduction.

Home Office

It appears, although generally trivial, that when using the home office actual expense method, the home office can be included in UBIA since per Reg 1.199A-2(a)(3) it is “determined and reported” on the tax return.

Allocating UBIA

Where a taxpayer is a partner or shareholder the partnership or S corporation must allocate the UBIA among the shareholders and partners in the same manner as depreciation is allocated to the shareholder or partner. If the qualified property does not produce tax depreciation during the year (for example, property that has been held for less than 10 years but whose recovery period has ended):

-

In the case of a partnership, each partner's share of the UBIA of qualified property is based on how gain would be allocated to the partners if the qualified property were sold at fair market value in a hypothetical sale for cash.

-

In the case of an S corporation, each shareholder's share of the UBIA of the qualified property is based on the ratio of shares in the S corporation held by the shareholder over the total shares of the S corporation.

Depreciable Period

For this purpose the term depreciable period means the period beginning on the date the taxpayer first puts the property in service and ending on the later of:

-

10 years after the placed-in-service date or

-

The last day of the last full year of the applicable MACRS recovery period of the property (Code Sec. 199A(b)(6)(B)).

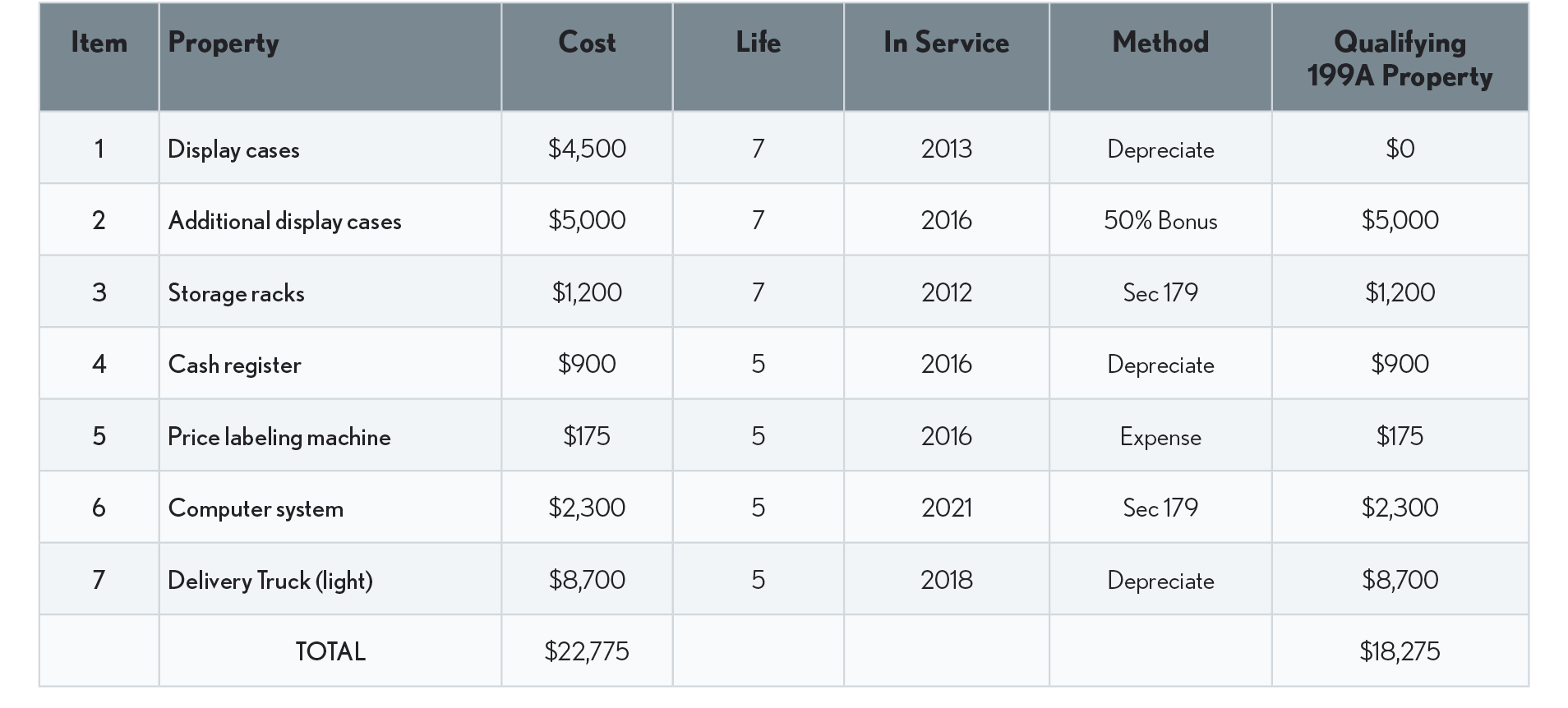

Example #7 – Retail Store - Gary has a retail store that he operates in rented retail space. His property that he used in his business during 2025 is listed in the table above.

When looking at the example, remember that the value we use for “qualifying 199A property” is the unadjusted basis. So, depreciation and expensing are ignored for this purpose. However, property counts as “qualifying property” within its depreciable life or 10 years, whichever is greater. Items 1, 4, 5 and 7 are past their useful lives but only #1 has been in service for a period greater than 10 years. So, all of Gary’s property except item #1 counts as “qualifying 199A property”. Thus, when the wage limitation is computed for Gary, the qualifying property used in the computation will be $18,275.

UBIA Example #8: Richard is a 25% shareholder in an S-Corporation that is not a specified service trade or business. During 2025 the S-corporation had $30,000 of qualified property it used during the year. Thus, when the wage limitation is computed for Richard, the qualifying property used in the computation will be $7,500 (25% of $30,000).

UBIA Example #9: Joyce owns a non-residential rental property (39-year recovery period). She originally purchased the property 12 years ago for $500,000 and the land value was $200,000. $300,000 ($500,000 - $200,000) would be the qualified property value for Joyce’s rental property.

Real Estate Investment Trust (REIT)

Sec 199A also includes qualified REIT dividends as pass-through income. However, for this purpose qualified REIT dividends do not include any portion of a dividend received from an REIT that is a capital gain dividend or qualified dividend. On Form 1099-DIV the eligible amount is in box 5.

Qualified Publicly Traded Partnership Income

The term "qualified publicly traded partnership income" means, with respect to any qualified trade or business of a taxpayer, the sum of:

-

The net amount of such taxpayer's allocable share of each qualified item of income, gain, deduction, and loss (as defined in Sec 199A(c)(3) and determined after the application of Sec 199A(c)(4) from a publicly traded partnership with pass-through income (Sec 7704(c)), and,

-

Any gain recognized by such taxpayer upon disposition of its interest in such partnership to the extent such gain is treated as an amount realized from the sale or exchange of property other than a capital asset under Sec 751(a) (unrealized receivables of the partnership).

REITS and Publicly Traded Partnerships

The regulations make it clear that the 199A computation for REITS and publicly traded partnerships (PTPs) is separate from that of the other 199A computations and has no effect on the other’s computation. Thus, should the QBI from REITS and PTPs be negative, the result will be a separate loss carryover and will have no effect on the taxpayer’s computation of the business entity 199A deduction.

Cooperative Dividends

Cooperatives must provide the necessary information to their patrons on Form 1099-PATR or an attachment to help eligible patrons figure their deduction. See the Instructions for Form 1120-C, U.S. Income Tax Return for Cooperative Associations, for rules applicable to agricultural and horticultural cooperatives

Qualified Trade or Businesses

Now we can continue our study of QTB and learn how to apply the wage limitation to QBI from QTBs.

So even though a taxpayer’s 1040 taxable income is above the phaseout cap, they can still get a Sec 199A deduction for a QTB so long as the business entity paid wages and/or has UBIA from qualified property. Those are the elements that make up the wage limitation.

Wage Limitation Through 2025

When a taxpayer’s 1040 taxable income exceeds the phaseout cap the preliminary QBI deduction is limited to the lesser of 20% of QBI or the wage limitation. The wage limitation is the greater of:

-

50% of the W-2 wages that the business paid, or,

-

25% of the W-2 wages from the business plus 2.5% of the unadjusted basis of the business’s qualified property.,

However, this limitation is phased in for taxpayers whose taxable income is between the threshold and the cap, resulting in a rather complicated calculation. So, we will study the limitation as it applies to taxpayers whose taxable income exceeds the phaseout cap and rely on the worksheet for those with 1040 taxable incomes between the threshold and the phaseout cap. We start with a taxpayer that is an S corporation stockholder:

Example #10 – Taxable Income Above the Phaseout Cap - Note this example uses 2023 rates - Therese, who is married and filing a joint return, is an active shareholder (meaning she works in the business and is not simply an investor) in an S corporation and owns 40% of the stock in the corporation. For 2023 she receives a W-2 in the amount of $250,000 as her compensation for working in the business and a K-1 that includes her flow-through income, QBI, of $150,000. Her taxable income (AGI less standard or itemized deductions) from her 1040 is $500,000, which is above the $494,600 cap, so she is subject to the wage limitation. The corporation paid $600,000 in wages during the year, which includes the $250,000 paid to her, and had $100,000 of qualified property. So, her 199A deduction is determined as follows:

-

Summary:

QBI = $150,000

Her share of Wages = $240,000 (40% of $600,000)

Her share of qualified property = $40,000 (40% of $100,000)

20% of her QBI = $30,000

50% of her share of the wages = $120,000 (50% of $240,000)

25% of her share of the wages = $ 60,000 (25% of $240,000)

2.5% of the qualified property = $1,000 (2.5% of $40,000)

The preliminary 199A deduction is limited for this activity to the lesser of 20% of QBI ($30,000) or the greater of:

• 50% of the W-2 wages from the business ($120,000) or

• 25% of the W-2 wages ($60,000) from the business plus 2.5% of the unadjusted basis of the business’s qualified property ($1,000), which totals $61,000.

$120,000 is greater than $61,000 so the preliminary 199A deduction for this entity is the lesser of the $120,000 W-2 limitation or $30,000; thus, the deduction is $30,000.

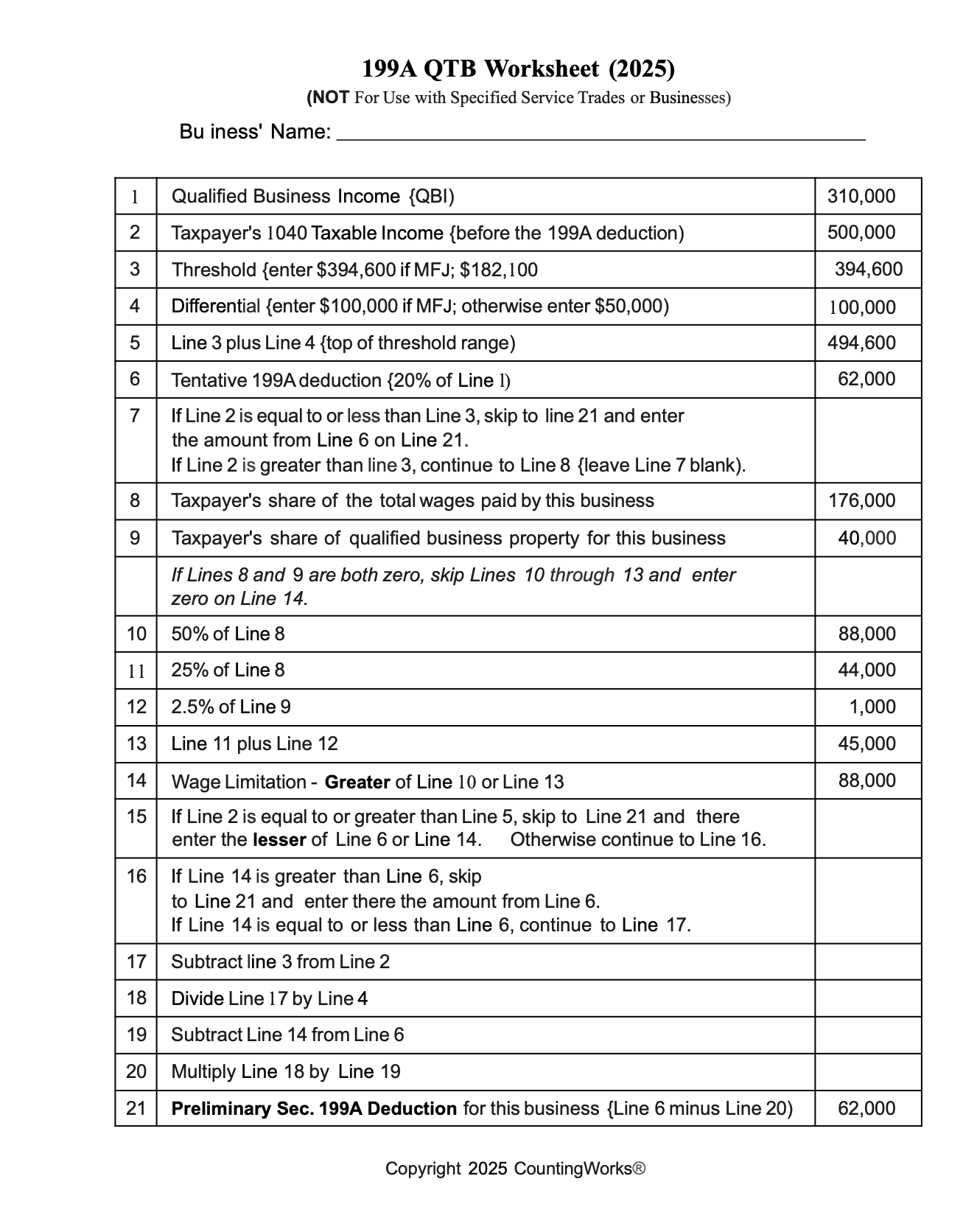

Example #11 – Wages Adjusted - But what would have been the result if Therese had taken a W-2 salary of only $90,000 instead of $250,000 and the difference ($160,000) had been added to her QBI (flow-through income). Her QBI would be $310,000 ($160,000 + $150,000). The wages paid by the S-corporation would drop to $440,000 ($600,000 - $160,000). The qualified property would remain the same and we have a substantially different result.

-

Summary:

QBI = $310,000. Her share of Wages = $176,000 (40% of $440,000)

Her share of qualified property = $40,000 (40% of $100,000)

20% of her QBI = $62,000

50% of her share of the wages = $88,000 (50% of $176,000)

25% of her share of the wages = $44,000 (25% of $176,000)

2.5% of the qualified property = $1,000 (2.5% of $40,000)

So, the preliminary deduction is limited to the lesser of 20% of QBI ($62,000) or the greater of:• 50% of the W-2 wages from the business ($88,000) or

• 25% of the W-2 wages ($44,000) from the business plus 2.5% of the unadjusted basis of the business’s qualified property ($1,000), which totals $45,000.

$88,000 is greater than $45,000 so the preliminary 199A deduction for this entity is the lesser of the $88,000 W-2 limitation or $62,000; thus, the preliminary deduction is $62,000.

Example #12 – Different Results for Different Taxpayer - Consider also that the S corporation that Therese was a shareholder in had other shareholders that were drawing a W-2 wage. If they also shifted more of their wages to pass-through income, the S corporation’s wages could be reduced to the point that the wage limitation might become the limiting factor. Consider further if the shareholders were the only employees and they all took no W-2 salary, the W-2 limitation would be the 2.5% of qualified property and the maximum 199A deduction would be $2,500 (2.5% of $100,000) split between them.

-

Caution

Reasonable compensation is not an amount determined to suit the best tax advantages of the stockholder. It is based on the facts and circumstances of the situation such as what others are paid for doing the same job, cost of living in the area and a number of other factors. See later in this guide for further discussion of reasonable compensation as it applies to the Sec 199A deduction.

K-1 Pass Through Data

Where a taxpayer has an interest in a pass-through activity, the K-1 from the activity, along with any required attachment, will provide the necessary data to compute the 199A deduction for the activity.

If you are the tax preparer receiving a K-1, as opposed to the one who is preparing the K-1, you are not responsible for making the decision of whether the business entity is a qualified trade or business, or a specified service trade or business.Those determinations are made at the entity level, and you as the preparer simply use the information provided with the K-1.The K-1 or an attachment to the K-1 should show the owner’s (stockholder, partner, or beneficiary) share of the information required to compute the 199A deduction for that particular entity.

If the K-1 or attachment

doesn’t include the owner’s (taxpayer’s) share of the required data, the

owner’s share will be presumed to be zero. (Reg. Sec. 1.199A-6(b)(iii))

Instructions: This worksheet is designed to determine the preliminary 199A deduction for a single business activity. However, it cannot be used for specified service trades or businesses. The results of this worksheet must be combined with the results from other businesses and flow-through income of the taxpayer to determine the combined preliminary Sec 199A deduction for the taxpayer. The combined preliminary Sec 199A deduction is further limited to 20% of the adjusted taxable income of the taxpayer.

CountingWorks has a separate worksheet for use with specified service trades or businesses. Although we believe the worksheets compute the deduction correctly, ultimately, the IRS worksheets or forms will take precedence.

Observations:

-

For S corporations, planning to maximize the 199A deduction becomes a balancing act between wages and QBI while walking a tightrope with the reasonable compensation issue.

-

Just as a reminder, the 199A deduction is figured at the individual, partner or stockholder level. In our Therese examples above, the stockholders other than Therese might have taxable incomes below the threshold and would not be subject to the W-2 limitation.

-

If the business in the examples above had been a partnership, the net profit would have flowed through to the individual partners as QBI. Where the partnership has no employees and no qualified property the W-2 limitation would be zero, and those partners with taxable income above the cap would have no 199A deduction (those between the threshold and cap would a get a partial 199A deduction). The same would apply to a sole proprietorship with no W-2 wages or qualified property.,

-

That brings up another conflicting issue: employee or independent contractor? Before TCJA, many smaller employers wanted to treat workers as independent contractors as opposed to employees to avoid payroll taxes, reporting and ACA issues. But keep in mind payments to independent contractors don’t count in the wage limitation and can have an effect on the 199A deduction.

-

On the other hand, there are individuals who are currently treated as employees who would like to be independent contractors for any number of reasons, some legitimate and some not. But the primary issues include:

-

They have substantial employee business expenses and can no longer deduct them.

-

They would like to benefit from the 199A deduction.

-

Of course, there are negatives: Paying SE tax instead of only the employee share of the FICA and giving up whatever fringe benefits the employer might offer.

At the end of the day, though, whether an individual is an employee, or an independent contractor comes down to the facts and circumstances of the situation, and not which status the individual prefers.

Congress, rather than having a step function, established a gradual transition to the W-2 limitation between the threshold and the cap.

In order to do this, they had to phase-out the 20% of QBI deduction and phase-in the W-2 limitation. This computation is best understood by example.

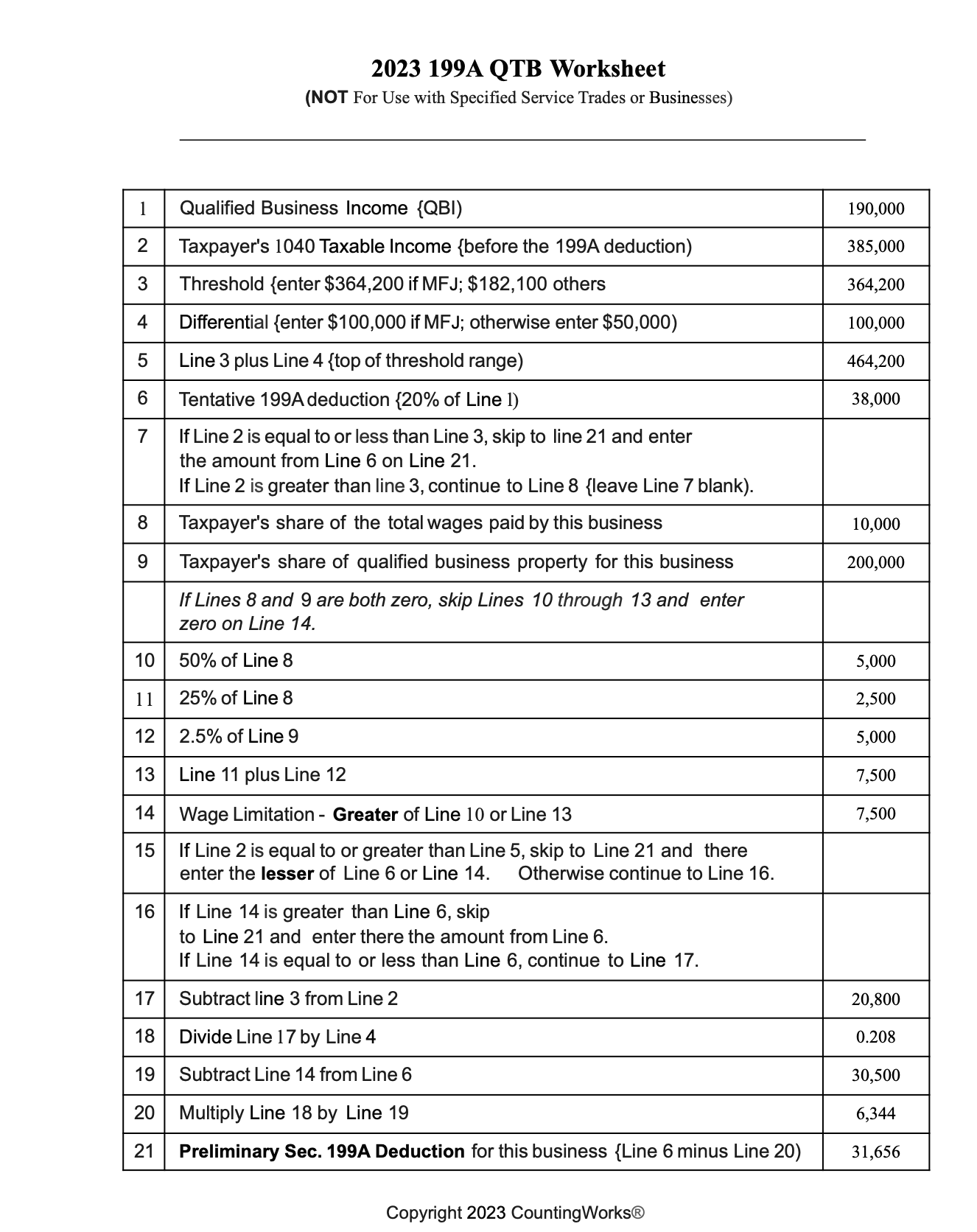

QTB-Example #13 - Taxable Income Between Threshold and Cap - In this example we have a taxpayer filing a joint return. - Note: this example uses 2023 amounts

-

Taxable Income (TI): $385,000

Threshold: $364,200

Differential: $100,000

QBI: $190,000

Tentative 199A deduction: $38,000 (20% of $190,000)

W-2 Wages paid by business: $10,000

Qualified Property: $200,000

a. 50% of Wages: $5,000 (50% of $10,000)

b. 25% of Wages: $2,500 (25% of $10,000)

c. 2.5% of Qualified Property: $5,000 (2.5% of $200,000)

d. Wage Limitation: Greater of a. or (b. + c.) = $7,500

e. Difference between TI and Threshold = $20,800

f. Divide e. by the differential = .208 (20,800/$100,000)

g. Tentative 199A deduction less Wage Limitation = $30,500 ($38,000 - $7,500)

h. Phase-out = f. times g. = $6,344 (.208 x $30,500)

i. Preliminary Section 199A deduction:

Tentative 199A deduction less h. = $31,656 ($38,000 – $6,344)

QBI Reductions for AGI Adjustments - The final regulation §1.199A-3(b)(1)(vi) (page 43-44 final regs) specifies that solely for the determination of QBI from a trade or business, the following are included as deductions from gross income when determining the activity’s QBI.

-

Self-employment tax deduction under Sec. 164(f)

-

Self-employed health insurance deduction under Sec 162(l), and

-

Deduction for qualified retirement plans under Sec 404.

QBI Adjustments Issues

-

Charitable contributions under Sec 170 – Sec 199A(c)(1) defines QBI as the net amount of qualified items of income, gain, deduction, and loss with respect to any qualified trade or business of the taxpayer and Sec 199A(c)(3) defines the term “qualified items of income, gain, deduction, and loss” to mean items of income, gain, deduction, and loss to the extent such items are effectively connected with the conduct of a trade or business within the U.S. Initially the IRS’ interpretation of that was that a charitable contribution made at the partnership level would reduce QBI, even though the charitable contribution is passed through separately to the partners. However, the Form 8995 instructions for 2020 and 2021 do not include charitable contributions as one of the items reducing QBI.

-

Unreimbursed partnership expenses under Sec 162 – There is a provision where partners may separately deduct unreimbursed partnership expenses on the Schedule E, line 28, column (g) and enter “UPE” in column (a) provided the partnership agreement requires the partner to pay the expenses. When a partner takes such a deduction, the partner must reduce the QBI from the partnership by the amount of the expenses deducted,,

-

Interest expense on purchase debt financing - Where a partner or S corp. stockholder financed the purchase of the entity, the interest on that debt is deductible on a separate line of Schedule E, column II labeled “business interest” and the name of the partnership or S corporation (Schedule E Instructions Line 28). These amounts reduce the QBI.

-

Business Interest Expense Limitation under Sec 163(j) – Where a business does not meet the inflation adjusted income exception amount of $25M ($31M for 2025, $29 million for 2024) the amount of deductible interest is limited under Sec 163(j) Limiting the interest deduction has the effect of increasing the QBI, leading one to question if the entire amount of interest should be used when computing QBI for the 199A deduction., The flow chart on page 6 of 2024 Form 8995, item #4, indicates the answer to that question is no.,

Allocation Requirement

Where an individual has multiple activities with qualified business income (QBI) the foregoing adjustments to AGI are proportionately allocated among the business activities.

Farming Activities and Horticultural Cooperatives

Cooperatives

As the law was originally written, some farmers would have been allowed an overly generous and unfair deduction of 20% of their qualified cooperative dividends, calculated on a gross basis. This was referred to as the “grain glitch” and was fixed by the Consolidated Appropriations Act, 2018. With the fix, the deduction for a specified agricultural cooperative is calculated and passed through to patrons under the rules for the domestic production activities deduction (DPAD) that existed before the repeal of Code Sec. 199. Thus, the cooperative’s deduction is generally 9% of the lesser of its taxable income, or its qualified production activities income, but limited to 50% of the co-op’s W-2 wages paid that are properly allocable to domestic production gross receipts. Some or all of the co-op’s deduction may be passed through to its patrons (the farmers), which then reduces the patron’s general QBI deduction. The cooperative must provide its patrons with the necessary information on Forms 1099-PATR or an attachment so each patron can figure their deduction. Starting with 2019 this is done on Schedule D of Form 8995-A. Note: The Form 1099-PATR (2020 and later years) includes several boxes that provide the needed information

Final regulations (T.D. 9947) governing the QBI deduction for Specified Agricultural Cooperatives and their patrons. largely adopt proposed regs issued in 2019 (NPRM REG-118425-18). The final regs are effective on January 14, 2021.

Farming Activities

Other than co-op related, are treated the same as any other QTB when computing the 199A deduction.

What About Multiple Business Activities with QBI?

The preliminary 199A deduction must be determined separately for each individual entity of a taxpayer and the various limitations and restrictions are applied at that level. Then all of the preliminary 199A deductions from the taxpayer’s sources are combined and limited to 20% of the taxpayer’s taxable income reduced by net capital gains.