Optional (ADS) Method for Personal & Real Property

Find details about the IRS's optional (ADS) method for personal and real property under the Modified Accelerated Cost Recovery System (MACRS).

Taxpayers who place in service personal property after 12/31/86 may elect to use the alternative depreciation system on a class-by-class basis, but the election is only available on a property-by property basis for residential rental and non-residential real property. The election is irrevocable and must be made by the extended due date of the tax return for the year the property is placed in service. ADS generally uses the straight-line method of computation and no salvage value.

Exception: For alternative minimum tax purposes, use 150% declining balance for personal property being depreciated under regular MACRS 200% or 150% declining-balance method.

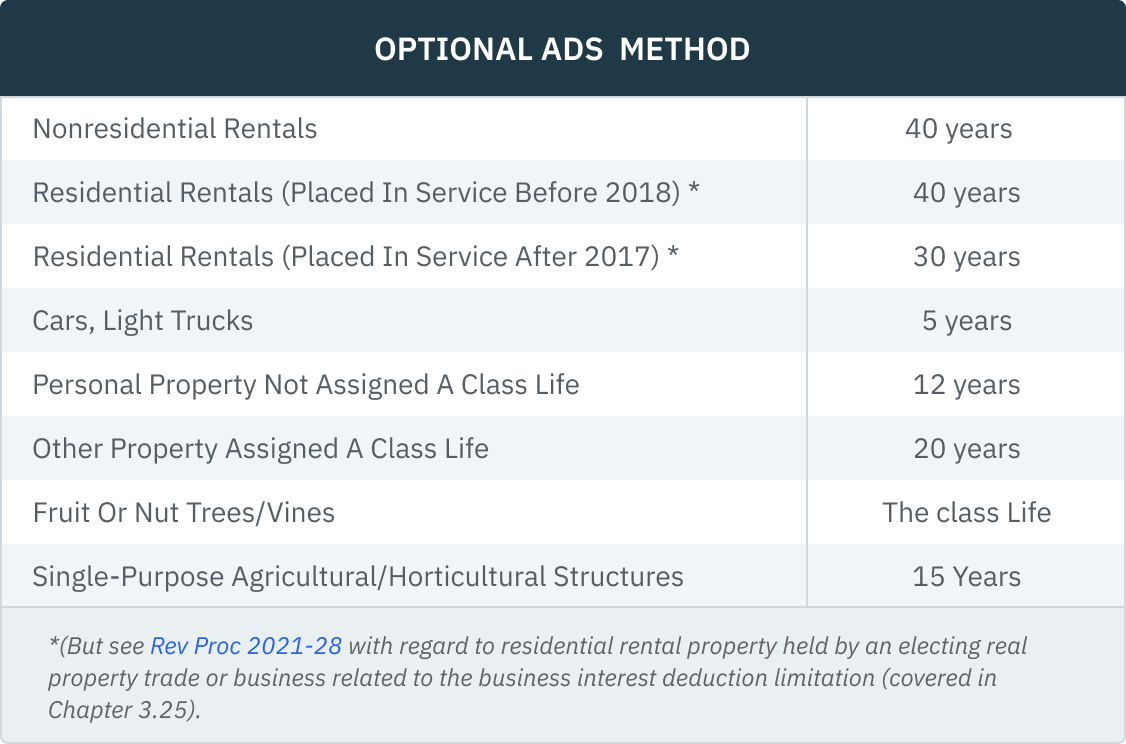

Like MACRS, ADS uses the half-year, mid-month, and mid-quarter conventions. Examples of recovery periods under ADS include: