Transmittal Form 1094-C

A 1094-C transmittal form must be used when filing 1095-Cs. Multiple 1094-Cs can be filed for an employer where all of the 1095-Cs were not filed with a single transmittal form.

Authoritative Transmittal Form

An Authoritative Transmittal is one that includes all parts of the 1094-C completed. The reason for this is that multiple 1094-Cs can be filed, but one of them must have all required parts completed while the others only require Part I to be completed.

Electronic Filing Requirement

In the past, an employer was required to file electronically if filing 250 or more 1095-Cs. The requirement applied separately to each type of form (e.g., 1099-NEC, 1095-C,1099-INT, etc.). However, in June 2018 the IRS proposed regulations that would change the non-aggregation rule so that all information returns, regardless of type, would need to be counted when determining whether the return threshold for required electronic filing is met. The IRS has adopted final regulations that lower the number of information reporting forms, such as the 1095-C, for the electronic filing threshold from 250 to 10, for returns required to be filed during calendar years on or after January 1, 2024. Proposed regulations that would have reduced the filing threshold from 250 to 100 for forms required to be filed in 2022 and 2023 were not adopted. (NPRM REG-102951-16, July 2021; TD 9972, Feb. 22, 2023)

Extension

Form 8809 must be filed by the due date of the 1094-C to obtain an automatic 30-day extension.

Electronic Filing Waiver

Form 8508, is used to request a waiver from filing information returns electronically. It must be filed at least 45 days before the due date of the returns.

Electronic Filing Penalty

Employers may be subject to a per-return penalty for failing to file electronically when required to do so. This amount is inflation-adjusted and is $310 for returns required to be filed in 2024 (Rev Proc 2022-38)

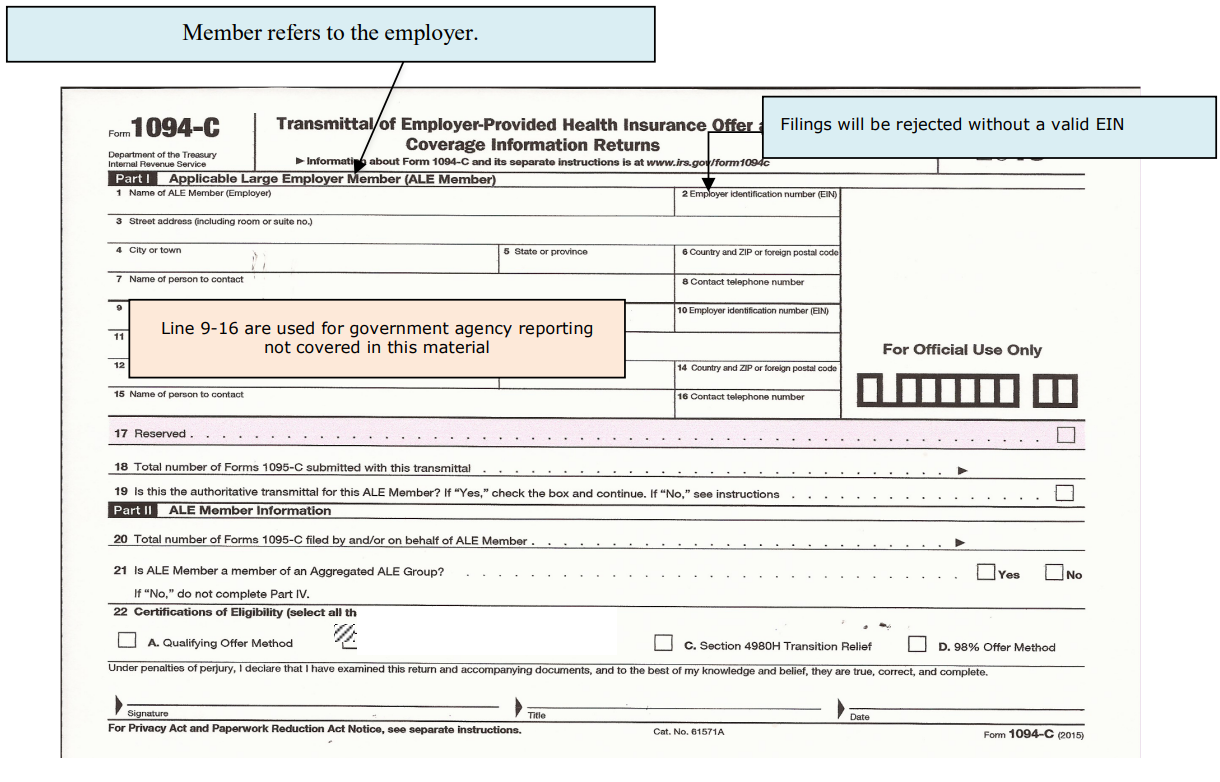

Definitions for Line 22 – Boxes A and D

Qualifying Offer:

A qualifying offer is an offer by an ALE of minimum essential coverage to one or more of its fulltime employees for all months (not within a limited non-assessment period) of the year for which the employee was a full-time employee:

-

Not costing more than 9.12% (2023) of the mainland single federal poverty line for the employee, and

-

Minimum essential coverage to the employee’s spouse and dependents.

If the employee does not have a spouse or dependent the employer is treated as if the employee did have a spouse or dependent for purposes of meeting the qualified offer.

Alternative Method of Completing Form 1095-C under the Qualifying Offer Method - If the employer reports using this method, it must not complete Form 1095-C, Part II, line 15, for any month for which a Qualifying Offer is made. Instead, it must enter the Qualifying Offer code 1A on Form 1095-C, line 14, for any month for which the employee received a Qualifying Offer (or in the all 12 months box if the employee received a Qualifying Offer for all 12 months), and must leave line 15 blank for any month for which code 1A is entered on line 14.

An employer is not required to use the Qualifying Offer Method, even if it is eligible and instead may enter on line 14 the applicable offer code and then enter on line 15 the dollar amount required as an employee contribution for the lowest-cost employee-only coverage providing minimum value for that month. See the Form 1094-C instructions for additional details.

98% Offer Method:

To be eligible for the 98% Offer Method, an employer must certify that the employer offered affordable (meets one of the Section 4980H safe harbors) coverage to 98% of its employees (not just full time) for all months of the year except for limited non-assessment periods (new employee waiting period) and offered dependent coverage.

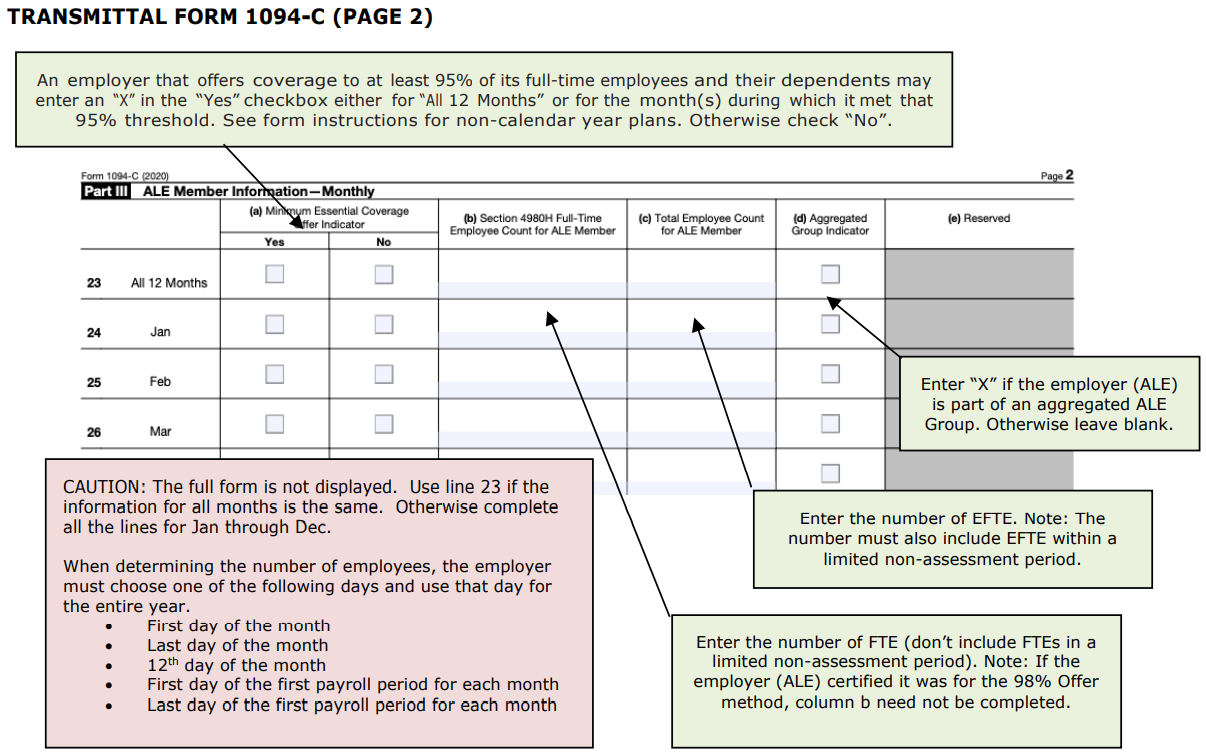

To ensure compliance with the general reporting rules, an employer should confirm for any employee for whom it fails to file a Form 1095-C that the employee was not a full-time employee for any month of the calendar year.

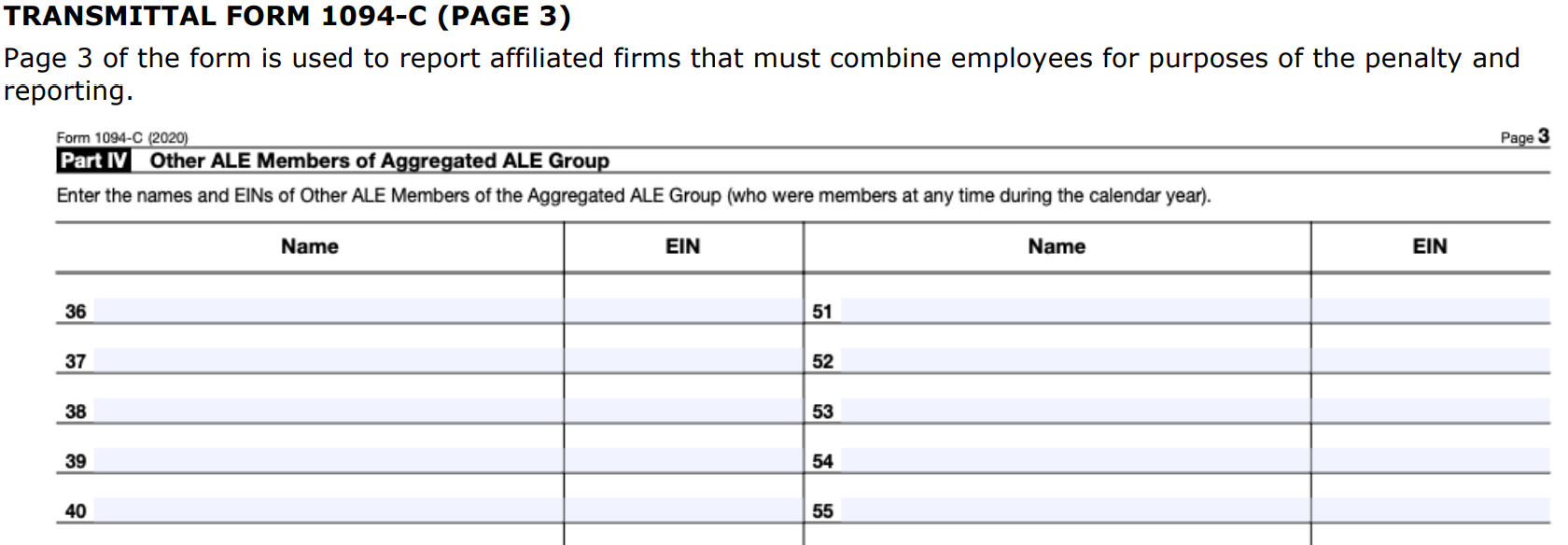

Corrected Filings

-

1094-C (Authoritative Filing) – File a standalone corrected 1094-C correcting the authoritative information filed on the original 1094-C and check the corrected box., Do not include any 1095-Cs with the corrected authoritative 1094-C.

-

1095-C – Include the corrected 1095-C (with the corrected box checked) and file with 1094-C (without the corrected box checked) and only complete Part I of the 1094-C.